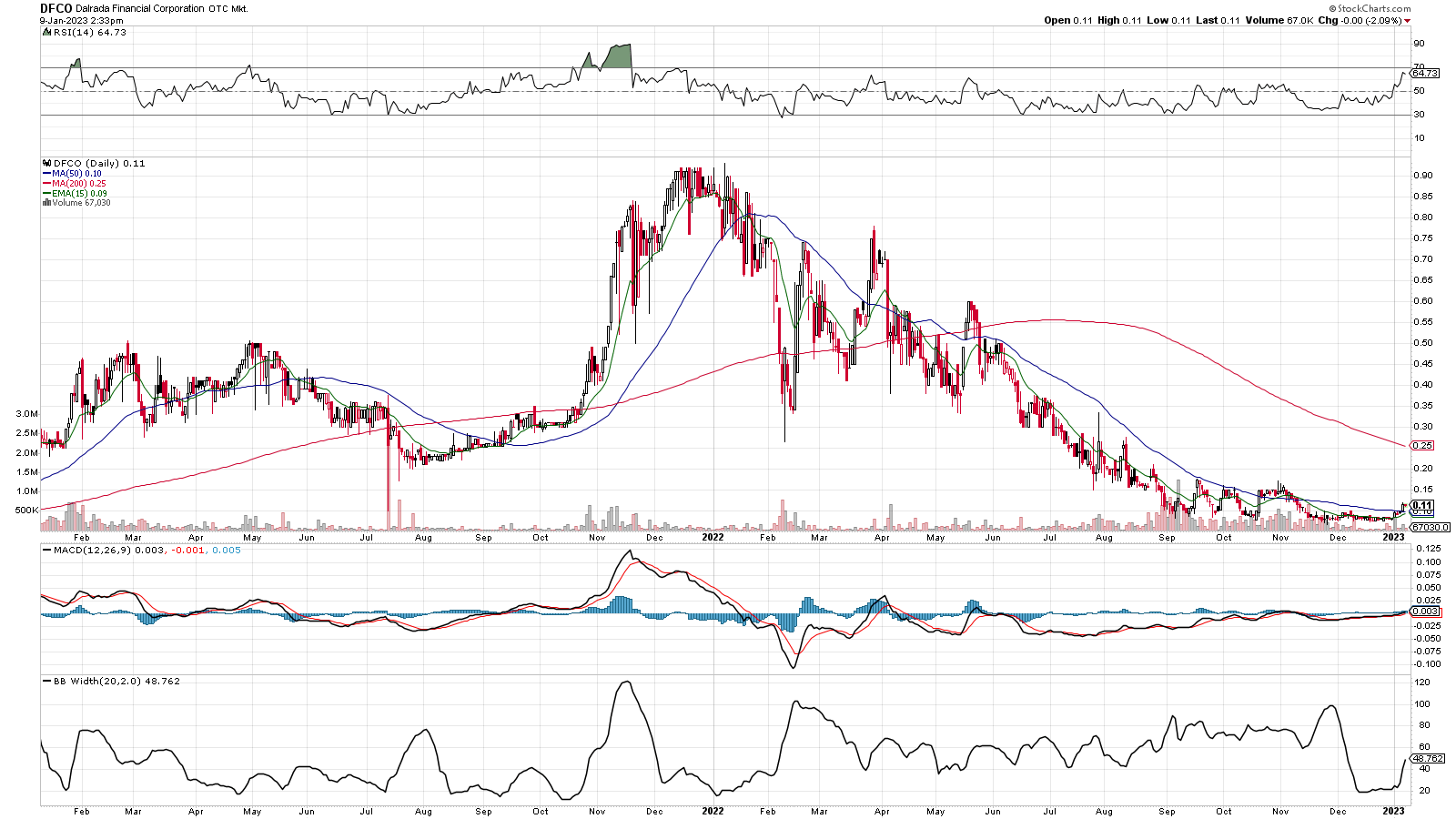

Back on July 18, 2019 I posted this article stating why I thought going long $DFCO was a good idea. The main emphasis was, in my eyes, the chart was overwhelmingly strong and primed for a big breakout, and the company was seemingly starting to come back from the dead. The pps was around .04 back then and since then it hit as high as .92, and even now after a miserable 2022 the pps is still up almost 200% from that level.

In the midst of the 2022 correction I then wrote this article, which highlighted why I thought that $DFCO was once again a very intriguing buy consideration, and that was when the pps was in the low .30s. Fast forward about 6 months and the current pps is now around .11, so anyone who bought the low .30s on my recommendation probably hates me. I certainly didn’t think we’d see the correction hit this low of a price level, but in the grand scheme it hasn’t changed my opinion and these prices make it all the more of a screaming buy.

The company had to dilute their outstanding shares in 2021 to further fund their growth, which in the OTC can often be the beginning of a death spiral for the share price as many companies need to opt for very toxic financing. Since their rebirth in 2018, Bonar and co. have been abnormally responsible (by OTC standards) with their dilution and though the o/s has *roughly* doubled (ballpark) since 2018, the amount of growth they’ve managed to build with that financing is incredible. The dilution in 2021 took the o/s from roughly 70 million to about 85 million where it now sits, and from what I can gather from the SEC filings and from watching the L2s trade, the dilution should be all but done.

Think about that. In 2021, the o/s grew by a little over 20%, but the share price fell from .90 to under .08, so over 90% loss! While the share price was declining, the fundamentals have gotten better quarter over quarter, and the company is primed for immense growth with relatively very little dilution having taken place. To put it another way, the market has severely overreacted and this is a ticking time bomb to the upside at this market cap.

With dilution being all but finished for now, the temporary ceiling that was holding the pps down is now lifted, and after a massive correction in 2022 the chart is fully reset and in fact is heavily oversold by my estimations. The market (at this current market cap) isn’t coming anywhere near pricing in the potential this company now has, and with dilution being finished we have a perfect storm to breakout in. The sentiment has been overdone to the downside, the chart is heavily oversold, the dilution is over, the news and future catalysts on the horizon are bigger than ever yet haven’t been priced in and there’s a very good chance that there are short positions that are now going to need to be covered at this stage.

The dilution seemingly wrapped up right around the new year and since then the pps has begun to float slightly higher, with the current price now sitting above the 50 day MA. .15 – .17 looks to be the next key level of resistance, so watch out when the price breaks above that level with strong volume backing it. That should be the next key technical trigger to watch out for, and especially if it’s tied to any sort of good news. There’s a lot on the horizon to look out for, especially tied to the Likido heat pumps and the GSA program update. The fiscal quarter that just wrapped up and this current one are strong candidates to see some big revenue growth as well.

Add everything up and I think 2023 is going to be a huge year for $DFCO, and this current price level around .11 is a no brainer in terms of risk vs reward and it’s high probability of success.